10-Q: Quarterly report [Sections 13 or 15(d)]

Published on April 27, 2026

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-Q

Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

For the quarterly period ended March 31, 2026

or

| Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

Commission File Number: 001-09819

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||||||||

| (Registrant’s telephone number, including area code) | ||||||||||||||||||||

| Securities registered pursuant to Section 12(b) of the Act: | ||||||||||||||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | ||||||||||||||

| ☒ | No | ☐ | ||||||||||||

| Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | ||||||||||||||

| ☒ | No | ☐ | ||||||||||||

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act. | ||||||||||||||

| ☒ | Accelerated filer | ☐ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐ | ||||||||||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

On April 24, 2026, the registrant had 215,150,907 shares outstanding of common stock, $0.01 par value, which is the registrant’s only class of common stock.

DYNEX CAPITAL, INC.

FORM 10-Q

INDEX

| Page | |||||||||||

PART I. FINANCIAL INFORMATION | |||||||||||

| Item 1. | Financial Statements | ||||||||||

Consolidated Balance Sheets as of March 31, 2026 (unaudited) and December 31, 2025 | |||||||||||

Consolidated Statements of Comprehensive Income (Loss) for the three months ended March 31, 2026 (unaudited) and March 31, 2025 (unaudited) | |||||||||||

Consolidated Statements of Shareholders' Equity for the three months ended March 31, 2026 (unaudited) and March 31, 2025 (unaudited) | |||||||||||

Consolidated Statements of Cash Flows for the three months ended March 31, 2026 (unaudited) and March 31, 2025 (unaudited) | |||||||||||

Notes to the Consolidated Financial Statements (unaudited) | |||||||||||

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | ||||||||||

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | ||||||||||

| Item 4. | Controls and Procedures | ||||||||||

PART II. OTHER INFORMATION | |||||||||||

| Item 1. | Legal Proceedings | ||||||||||

Item 1A. | Risk Factors | ||||||||||

Item 2. | Unregistered Sale of Equity and Use of Proceeds | ||||||||||

Item 3. | Defaults Upon Senior Securities | ||||||||||

Item 4. | Mine Safety Disclosures | ||||||||||

| Item 5. | Other Information | ||||||||||

| Item 6. | Exhibits | ||||||||||

| SIGNATURES | |||||||||||

PART I. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

CONSOLIDATED BALANCE SHEETS

($s in thousands except per share data)

| March 31, 2026 | December 31, 2025 | ||||||||||

| ASSETS | (unaudited) | ||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Cash collateral posted to counterparties | |||||||||||

Mortgage-backed securities (including pledged assets of $ | |||||||||||

Due from counterparties | |||||||||||

| Derivative assets | |||||||||||

| Accrued interest receivable | |||||||||||

Other assets | |||||||||||

| Total assets | $ | $ | |||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY | |||||||||||

| Liabilities: | |||||||||||

| Repurchase agreements | $ | $ | |||||||||

Due to counterparties | |||||||||||

| Derivative liabilities | |||||||||||

| Cash collateral posted by counterparties | |||||||||||

| Accrued interest payable | |||||||||||

Dividends payable | |||||||||||

| Other liabilities | |||||||||||

| Total liabilities | |||||||||||

| Shareholders’ equity: | |||||||||||

Preferred stock, par value $ | |||||||||||

Common stock, par value $ | |||||||||||

| Additional paid-in capital | |||||||||||

| Accumulated other comprehensive loss | ( | ( | |||||||||

| Accumulated deficit | ( | ( | |||||||||

| Total shareholders’ equity | |||||||||||

| Total liabilities and shareholders’ equity | $ | $ | |||||||||

See notes to the unaudited consolidated financial statements.

1

DYNEX CAPITAL, INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(UNAUDITED)

($s in thousands except per share data)

| Three Months Ended | |||||||||||

| March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| INTEREST INCOME (EXPENSE) | |||||||||||

| Interest income | $ | $ | |||||||||

| Interest expense | ( | ( | |||||||||

Net interest income | |||||||||||

| OTHER GAINS (LOSSES) | |||||||||||

Realized gain on sales of investments, net | |||||||||||

| Unrealized (loss) gain on investments, net | ( | ||||||||||

| Gain (loss) on derivative instruments, net | ( | ||||||||||

Total other gains (losses), net | ( | ( | |||||||||

| EXPENSES | |||||||||||

| Compensation and benefits | ( | ( | |||||||||

| Other general and administrative | ( | ( | |||||||||

| Other operating expenses | ( | ( | |||||||||

| Total operating expenses | ( | ( | |||||||||

| Net loss | ( | ( | |||||||||

| Preferred stock dividends | ( | ( | |||||||||

| Net loss to common shareholders | $ | ( | $ | ( | |||||||

| Other comprehensive income: | |||||||||||

| Unrealized (loss) gain on available-for-sale investments | $ | ( | $ | ||||||||

| Total other comprehensive (loss) income | ( | ||||||||||

| Comprehensive (loss) income to common shareholders | $ | ( | $ | ||||||||

| Weighted average common shares-basic | |||||||||||

| Weighted average common shares-diluted | |||||||||||

| Net loss per common share-basic | $ | ( | $ | ( | |||||||

| Net loss per common share-diluted | $ | ( | $ | ( | |||||||

See notes to the unaudited consolidated financial statements.

2

DYNEX CAPITAL, INC.

CONSOLIDATED STATEMENTS OF SHAREHOLDERS’ EQUITY

(UNAUDITED)

($s in thousands)

For the Three Months Ended March 31, 2026 | |||||||||||||||||||||||||||||||||||||||||

| Preferred Stock | Common Stock | Additional Paid-in Capital | Accumulated Other Comprehensive Loss | Accumulated Deficit | Total Shareholders’ Equity | ||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | ||||||||||||||||||||||||||||||||||||||

Balance as of December 31, 2025 | $ | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||||

| Stock issuance | — | — | — | — | |||||||||||||||||||||||||||||||||||||

Share-based compensation, net of amortization | — | — | — | — | |||||||||||||||||||||||||||||||||||||

| Adjustments for tax withholding on share-based compensation | — | — | ( | ( | ( | — | — | ( | |||||||||||||||||||||||||||||||||

| Stock issuance costs | — | — | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||

| Net loss | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||

| Dividends on preferred stock | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||

| Dividends on common stock | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||

| Other comprehensive loss | — | — | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||||||

Balance as of March 31, 2026 | $ | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||||

For the Three Months Ended March 31, 2025 | |||||||||||||||||||||||||||||||||||||||||

| Balance as of December 31, 2024 | $ | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||||

| Stock issuance | — | — | — | — | |||||||||||||||||||||||||||||||||||||

Share-based compensation, net of amortization | — | — | — | — | |||||||||||||||||||||||||||||||||||||

| Adjustments for tax withholding on share-based compensation | — | — | ( | ( | ( | — | — | ( | |||||||||||||||||||||||||||||||||

| Stock issuance costs | — | — | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||

| Net loss | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||

| Dividends on preferred stock | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||

| Dividends on common stock | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||

| Other comprehensive income | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||

| Balance as of March 31, 2025 | $ | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||||

See notes to the unaudited consolidated financial statements.

3

DYNEX CAPITAL, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

($s in thousands)

($s in thousands)

| Three Months Ended | |||||||||||

| March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| Operating activities: | |||||||||||

| Net loss | $ | ( | $ | ( | |||||||

Adjustments to reconcile net loss to cash provided by operating activities: | |||||||||||

Realized gain on sales of investments, net | ( | ||||||||||

| Unrealized loss (gain) on investments, net | ( | ||||||||||

| (Gain) loss on derivative instruments,net | ( | ||||||||||

| Amortization of investment premiums, net | |||||||||||

Other amortization and depreciation | |||||||||||

| Share-based compensation expense | |||||||||||

| Increase in accrued interest receivable | ( | ( | |||||||||

| Increase in accrued interest payable | |||||||||||

| Change in other assets and liabilities, net | ( | ( | |||||||||

Net cash provided by operating activities | |||||||||||

| Investing activities: | |||||||||||

| Purchases of investments | ( | ( | |||||||||

| Principal payments received on trading securities | |||||||||||

| Principal payments received on available-for-sale investments | |||||||||||

| Proceeds from sales of trading securities | |||||||||||

| Principal payments received on mortgage loans held for investment | |||||||||||

Net receipts (payments) on derivative instruments | ( | ||||||||||

(Decrease) increase in cash collateral posted by counterparties | ( | ||||||||||

| Net cash used in investing activities | ( | ( | |||||||||

| Financing activities: | |||||||||||

| Borrowings under repurchase agreements | |||||||||||

| Repayments of repurchase agreement borrowings | ( | ( | |||||||||

| Proceeds from issuance of common stock | |||||||||||

| Cash paid for stock issuance costs | ( | ||||||||||

| Payments related to tax withholding for share-based compensation | ( | ( | |||||||||

| Dividends paid | ( | ( | |||||||||

| Net cash provided by financing activities | |||||||||||

Net increase (decrease) in cash, including cash posted to counterparties | ( | ||||||||||

Cash including cash collateral posted to counterparties at beginning of period | |||||||||||

Cash including cash collateral posted to counterparties at end of period | $ | $ | |||||||||

| Supplemental Disclosure of Cash Activity: | |||||||||||

Cash paid for interest on repurchase agreements | $ | $ | |||||||||

Noncash Investing Activities: | |||||||||||

4

Payable for investments pending settlement | $ | $ | |||||||||

See notes to the unaudited consolidated financial statements.

5

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1 – ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Organization

Dynex Capital, Inc. (“Dynex” or the “Company”) is a real estate investment trust (“REIT”) structured to deliver dividends to shareholders supported by long term returns from investments in mortgage assets backed by U.S. housing and commercial real estate. The Company’s common stock and preferred stock trade on the New York Stock Exchange (“NYSE”) under the ticker symbols “DX” and “DXPRC”, respectively.

The Company is internally managed and primarily earns income from investing in residential and commercial mortgage-backed securities (“RMBS” and “CMBS”, respectively), which are backed by residential and commercial mortgage loans, and which are Agency securities guaranteed by U.S. government-sponsored enterprises (“GSEs”). The Company may also invest in other mortgage-related assets consistent with its objectives. Dynex actively manages interest rate, prepayment, spread, liquidity, and counterparty risks. The Dynex approach emphasizes risk management and disciplined capital allocation designed to preserve book value and support dividends across market cycles.

Basis of Presentation

Use of Estimates

Consolidation and Variable Interest Entities

The consolidated financial statements include the accounts of the Company and the accounts of its majority owned subsidiaries. All intercompany accounts and transactions have been eliminated in consolidation.

The Company did not consolidate any variable interest entities (“VIEs”) as of March 31, 2026. The Company consolidates a VIE if the Company is determined to be the VIE’s primary beneficiary, which is defined as the party that has both (i) the power to control the activities that most significantly impact the VIE’s financial performance; and (ii) the right to receive benefits or absorb losses that could potentially be significant to the VIE. The Company reconsiders its evaluation of whether to consolidate a VIE on an ongoing basis, based on changes in the facts and circumstances pertaining to the VIE. Though the Company invests in Agency and non-Agency MBS which are generally considered to be interests in VIEs, the Company does not consolidate these entities because it does not meet the criteria to be deemed the primary beneficiary. The maximum exposure to loss for these VIEs is the carrying value of the MBS.

6

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Income Taxes

The Company has elected to be taxed as a REIT under the Internal Revenue Code of 1986 (the “Tax Code”) and the corresponding provisions of state law. To qualify as a REIT, the Company must meet certain asset, income, ownership, and distribution tests. To meet these requirements, the Company’s main source of income is interest earned from obligations secured by mortgages on real property, and the Company must distribute at least 90% of its annual REIT taxable income to shareholders. The Company’s income will generally not be subject to federal income tax to the extent its income is distributed as dividends to shareholders.

The Company assesses its tax positions for all open tax years and determines whether the Company has any material unrecognized liabilities and records these liabilities, if any, to the extent they are deemed more likely than not to have been incurred.

Net Income (Loss) Per Common Share

The Company calculates basic net income (loss) per common share by dividing net income (loss) to common shareholders for the period by weighted-average shares of common stock outstanding for that period. Please see Note 2 for the calculation of the Company’s basic and diluted net income (loss) per common share for the periods indicated.

The Company currently has restricted stock, service-based restricted stock units (“RSUs”) and performance-based stock units (“PSUs”) issued and outstanding. Restricted stock awards issued under the Company’s 2020 Stock and Incentive Plan (the “2020 Plan”) are considered participating securities and therefore are included in the computation of basic net income per common share using the two-class method because holders of unvested shares of restricted stock issued are eligible to receive non-forfeitable dividends. Holders of RSUs and PSUs issued under the 2020 Plan as well as the Company’s 2025 Stock and Incentive Plan (the “2025 Plan”) accrue forfeitable dividend equivalent rights ("DERs") over the period outstanding, receiving dividend payments only upon the settlement date if the requisite service-based and performance-based conditions have been achieved, as applicable. As such, RSUs and PSUs are excluded from the computation of basic net income per common share but are included in the computation of diluted net income per common share using the treasury stock method unless the effect is to reduce a net loss or increase the net income per common share (also known as “anti-dilutive”). Upon vesting, restrictions on transfer expire on each share of restricted stock, RSU, and PSU, and each such share or unit becomes one unrestricted share of common stock and is included in the computation of basic net income per common share.

Because the Company’s 6.900% Series C Fixed-to-Floating Rate Cumulative Redeemable Preferred Stock (the “Series C Preferred Stock”) is redeemable at the Company’s option for cash only and convertible into shares of common stock only upon a change of control of the Company (and subject to other circumstances) as described in Article IIIC of the Company’s Restated Articles of Incorporation, as amended, the effect of those shares and their related dividends are excluded from the calculation of diluted net income per common share for the periods presented.

Cash and Cash Equivalents

Cash and cash equivalents include unrestricted demand deposits at highly rated financial institutions and highly liquid investments with original maturities of three months or less. The Company’s cash balances fluctuate throughout the year and may exceed Federal Deposit Insurance Corporation (“FDIC”) insured limits from time to time. Although the Company bears risk on amounts in excess of those insured by the FDIC, the Company believes the risk of loss is mitigated by the financial position, creditworthiness, and strength of the depository institutions in which those deposits are held.

Cash Collateral Posted To/By Counterparties

The Company regularly pledges and receives amounts to cover margin requirements related to the Company’s financing and derivative instruments. If the amount pledged to a counterparty exceeds the amount received from a counterparty, the net amount is recorded as an asset within “cash collateral posted to counterparties,” and if the amount received from a counterparty exceeds the amount pledged to a counterparty, the

7

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

net amount is recorded as a liability within “cash collateral posted by counterparties” on the Company’s consolidated balance sheets.

The following table provides a reconciliation of “cash” and “cash posted to counterparties” reported on the Company's consolidated balance sheet as of March 31, 2026 presented herein that sum to the total of the same such amounts shown on the Company’s consolidated statement of cash flows for the three months ended March 31, 2026:

($s in thousands) | March 31, 2026 | ||||

| Cash and cash equivalents | $ | ||||

| Cash collateral posted to counterparties | |||||

| Total cash including cash posted to counterparties shown on consolidated statement of cash flows | $ | ||||

Mortgage-Backed Securities

The Company’s MBS are recorded at fair value on the Company’s consolidated balance sheet. Changes in fair value of MBS purchased prior to January 1, 2021 are designated as available-for-sale (“AFS”) with changes in fair value reported in other comprehensive income (“OCI”) as an unrealized gain (loss) until the security is sold or matures. Effective January 1, 2021, the Company elected the fair value option (“FVO”) for all MBS purchased on or after that date with changes in fair value reported in net income as “unrealized gain (loss) on investments, net” until the security is sold or matures. Management elected the fair value option so that net income will reflect the changes in fair value for its future purchases of MBS in a manner consistent with the presentation and timing of the changes in fair value of its derivative instruments. Upon the sale of an MBS, any unrealized gain or loss within OCI or net income is reclassified to “realized gain (loss) on sale of investments, net” within net income using the specific identification method.

Interest Income, Premium Amortization, and Discount Accretion. Interest income on MBS is accrued based on the outstanding principal balance (or notional balance in the case of IO securities) and the contractual terms. Premiums or discounts associated with the purchase of MBS are amortized or accreted into interest income over the life of such securities using the effective interest method, and adjustments to premium amortization and discount accretion are made for actual cash payments received. On at least a quarterly basis, the Company reviews and makes any necessary adjustments to its cash flows and updates the yield recognized on these assets.

Determination of MBS Fair Value. The Company estimates the fair value of the majority of its MBS based upon prices obtained from an independent third-party pricing service. These prices are assessed for reasonableness using additional third-party pricing services. Please refer to Note 6 for further discussion of MBS fair value measurements.

Allowance for Credit Losses. On at least a quarterly basis, the Company evaluates any MBS designated as AFS with a fair value less than its amortized cost for credit losses. If the difference between the present value of cash flows expected to be collected on the MBS is less than its amortized cost, the difference is recorded as an allowance for credit loss through net income up to and not exceeding the amount that the amortized cost exceeds current fair value. Subsequent changes in credit loss estimates are recognized in earnings in the period in which they occur. Because the majority of the Company’s investments are higher credit quality and most are guaranteed by a GSE, the Company is not likely to have an allowance for credit losses related to its MBS recorded on its consolidated balance sheet.

Interest accrued between payment dates on MBS is presented separately from the Company’s investment portfolio as “accrued interest receivable” on its consolidated balance sheet. The Company does not estimate an allowance for credit loss for its accrued interest receivable because the interest is generally received within 30 days and amounts not received when due are written off against interest income.

Repurchase Agreements

The Company’s repurchase agreements are used to finance its purchases of MBS. The Company pledges its securities as collateral to secure a loan, which is equal to a specified percentage of the estimated fair value of the pledged collateral. The Company retains beneficial ownership of the pledged collateral. Pursuant to Accounting

8

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Standards Codification (“ASC”) Topic 860, the Company accounts for repurchase agreements as collateralized financing transactions, which are carried at their contractual amounts (cost), plus accrued interest. The interest rates the Company pays for these borrowings are based on a spread added to the Secured Overnight Funding Rate (“SOFR”). At the maturity of a repurchase agreement borrowing, the Company is required to repay the loan and concurrently receives back its pledged collateral from the lender, or, with the consent of the lender, the Company may renew the agreement at the then prevailing financing rate. A repurchase agreement lender may require the Company to pledge additional collateral in the event of a decline in the fair value of the collateral pledged. Repurchase agreement financing is recourse to the Company and the assets pledged. The repurchase facilities available to the Company are uncommitted with no guarantee of renewal.

Derivative Instruments

Derivative instruments are carried at fair value, and all periodic interest benefits/costs and changes in the fair value of derivative instruments, including gains and losses realized upon termination, maturity, or settlement, are recorded in “gain (loss) on derivative instruments, net” on the Company’s consolidated statements of comprehensive income (loss). Cash receipts and payments related to derivative instruments are classified in the investing activities section of the consolidated statements of cash flows in accordance with the underlying nature or purpose of the derivative transactions.

The Company’s short positions in U.S. Treasury futures contracts are centrally cleared through the Chicago Mercantile Exchange (“CME”), which requires the Company to post initial margin as determined by the CME. Daily variation margin is exchanged, typically in cash, for the changes in the fair value of the futures contracts, which is treated as legal settlement of the exposure under the related futures contracts as opposed to a pledge of collateral. The effect of these legal settlements reduces what would have otherwise been reported as the fair value of the futures contracts, generally to $0. The margin requirement varies based on the market value of the open positions and the equity retained in the account. Any margin excess or deficit outstanding is recorded as a receivable or payable within “due from/to counterparties” as of the date of the Company’s consolidated balance sheets. The Company realizes gains or losses on these contracts upon expiration at an amount equal to the difference between the current fair value of the underlying asset and the contractual price of the futures contract.

The Company’s interest rate swaps are pay-fixed, which involve the receipt of variable-rate amounts based on SOFR from a counterparty in exchange for the Company making fixed-rate payments over the life of the interest rate swap without exchange of the underlying notional amount. The net periodic interest benefit (cost) is recorded in the period earned (incurred) in “gain (loss) on derivative instruments, net”, but the net receipt (payment) of cash is exchanged annually, typically on the anniversary of each agreement’s effective date. Similar to the Company’s U.S. Treasury futures, interest rate swap agreements are centrally cleared through the CME with requirements to post initial margin and to exchange daily variation margin amounts, which are treated as legal settlements of the agreements. Any margin excess or deficit outstanding is recorded as a receivable or payable within “due from/to counterparties” as of the date of the Company’s consolidated balance sheets.

The Company’s interest rate swaptions are SOFR-based and provide the Company the right, but not the obligation, to enter into an interest rate swap at a predetermined notional amount with a stated term and pay and receive rates in the future. These agreements are entered into directly with a counterparty (a “bilateral contract”) with whom we may exchange margin collateral. Because these agreements are not centrally cleared, the Company has exposure to counterparty risk. The Company records the premium it will pay for the swaption as a derivative asset on its consolidated balance sheet and adjusts the balance for changes in fair value through “gain (loss) on derivative instruments” until the swaption is exercised or the contract expires. If the swaption expires unexercised, the realized loss is limited to the premium paid. If exercised, the realized gain or loss on the swaptions is equal to the difference between the fair value of the underlying interest rate swap and the premium paid.

The Company may also use options on U.S. Treasury futures, which are initially recorded at the price of the premium paid at inception. Subsequent changes in fair value are recorded in “gain (loss) on derivatives instruments” until the option is exercised or the contract expires. If the option expires unexercised, the realized loss is limited to the premium paid at inception. If exercised, the realized gain or loss on the option is equal to the difference between the fair value of the underlying U.S. Treasury future and the premium paid at inception.

The Company purchases to-be-announced (“TBA”) securities as a means of investing in non-specified

9

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

fixed-rate Agency RMBS and may also periodically sell TBA securities as a means of economically hedging its exposure to Agency RMBS. A TBA security is a forward contract (“TBA contract”) for the purchase (“long position”) or sale (“short position”) of a non-specified Agency MBS at a predetermined price with certain principal and interest terms and certain types of collateral, but the particular Agency securities to be delivered are not identified until shortly before the settlement date. The Company accounts for long and short positions in Agency RMBS TBAs as derivative instruments in accordance with ASC 815 because the Company cannot assert that it is probable at inception and throughout the term of an individual TBA transaction that its settlement will result in physical delivery of the underlying Agency RMBS or that the individual TBA transaction will settle in the shortest time period possible.

Share-Based Compensation

The Company’s 2025 Plan reserves for issuance up to 12,000,000 common shares for eligible employees, non-employee directors, consultants, and advisors to the Company to be granted in the form of stock options, restricted stock, RSUs, stock appreciation rights, PSUs, and performance-based cash awards (collectively, “awards”). Awards previously granted under the 2020 Plan will remain outstanding and valid in accordance with their terms, but no new awards will be granted under the 2020 Plan. As of March 31, 2026, there were 9,426,189 common shares remaining available for issuance under the 2025 Plan.

The Company has issued restricted stock and RSUs, which are treated as equity awards and recorded at their fair value using the closing stock price on the grant date. Compensation expense is generally recognized over a service period specified within each award with a corresponding credit to shareholders’ equity using the straight-line method until the vesting date specified within each award or until the employee becomes eligible for retirement, if earlier than the vesting date. Compensation expense is recognized immediately upon the grant date for equity awards granted to an employee who is retirement eligible.

The Company also has PSUs issued and outstanding which contain Company performance-based conditions. PSUs subject to Company performance-based conditions are initially recognized as equity at their fair value which is measured using the closing stock price on the grant date multiplied by the number of units expected to vest based on an assessment of the probability of achievement of the Company performance-based conditions as of the grant date. The grant date fair value is recognized as expense using the straight-line method until the earlier of the vesting date specified within each award or the date the employee becomes eligible for retirement. Adjustments are made, if necessary, based on any change in probability of achievement which is re-assessed as of each reporting date and on at least a quarterly basis.

The Company does not estimate forfeitures for any of its share-based compensation awards but adjusts for actual forfeitures in the periods in which they occur. Because RSUs and PSUs have forfeitable DERs, which are paid in cash only upon settlement, any accrued DERs on forfeited units are reversed with a corresponding credit to “Compensation and benefits” expense.

Contingencies

Recently Issued Accounting Pronouncements

The Company evaluates Accounting Standards Updates (“ASU”) issued by the Financial Accounting Standards Board on at least a quarterly basis to evaluate applicability and significance of any impact on its financial condition and results of operations. There are no new accounting pronouncements which are not yet effective that are expected to have a significant impact on our consolidated financial statements upon adoption.

10

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

NOTE 2 – NET INCOME (LOSS) PER COMMON SHARE

Please refer to Note 1 for information regarding the Company’s treatment of its preferred stock and stock awards in the calculation of its basic and diluted net income or loss per common share and to Note 7 for information regarding the Company’s stock award activity for the periods presented. The following table presents the computations of basic and diluted net income or loss per common share for the periods indicated:

| Three Months Ended | |||||||||||

| March 31, | |||||||||||

($s in thousands) | 2026 | 2025 | |||||||||

| Weighted average number of common shares outstanding - basic | |||||||||||

| Incremental common shares-unvested RSUs | |||||||||||

| Incremental common shares-unvested PSUs | |||||||||||

| Weighted average number of common shares outstanding - diluted | |||||||||||

| Net loss to common shareholders | $ | ( | $ | ( | |||||||

| Net loss per common share-basic | $ | ( | $ | ( | |||||||

| Net loss per common share-diluted | $ | ( | $ | ( | |||||||

The calculation of diluted net loss per common share for the three months ended March 31, 2026 and March 31, 2025 excludes unvested RSUs and PSUs of 1,303,235 and 547,845 , respectively, which would have been anti-dilutive for the period.

11

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

NOTE 3 – MORTGAGE-BACKED SECURITIES

The following tables provide details on the Company’s MBS by investment type as of the dates indicated:

| March 31, 2026 | |||||||||||||||||||||||

($s in thousands) | Agency RMBS | Agency CMBS | CMBS IO (1) | Total | |||||||||||||||||||

Measured at fair value through net income: | |||||||||||||||||||||||

Amortized cost | $ | $ | $ | $ | |||||||||||||||||||

Gross unrealized gain | |||||||||||||||||||||||

Gross unrealized loss | ( | ( | ( | ( | |||||||||||||||||||

Fair value through net income | $ | $ | $ | $ | |||||||||||||||||||

Measured at fair value through OCI: | |||||||||||||||||||||||

Amortized cost | $ | $ | $ | $ | |||||||||||||||||||

Gross unrealized gain | |||||||||||||||||||||||

Gross unrealized loss | ( | ( | ( | ( | |||||||||||||||||||

Fair value through OCI | $ | $ | $ | $ | |||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

| December 31, 2025 | |||||||||||||||||||||||

Agency RMBS | Agency CMBS | CMBS IO (1) | Total | ||||||||||||||||||||

Measured at fair value through net income: | |||||||||||||||||||||||

Amortized cost | $ | $ | $ | $ | |||||||||||||||||||

Gross unrealized gain | |||||||||||||||||||||||

Gross unrealized loss | ( | ( | ( | ( | |||||||||||||||||||

Fair value through net income | $ | $ | $ | $ | |||||||||||||||||||

Measured at fair value through OCI: | |||||||||||||||||||||||

Amortized cost | $ | $ | $ | $ | |||||||||||||||||||

Gross unrealized gain | |||||||||||||||||||||||

Gross unrealized loss | ( | ( | ( | ( | |||||||||||||||||||

Fair value through OCI | $ | $ | $ | $ | |||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

(1) The Company held a notional balance of Agency CMBS IO and non-Agency CMBS IO of $ | |||||||||||||||||||||||

The majority of the Company’s MBS are pledged as collateral for the Company’s repurchase agreements, which are disclosed in Note 4. Actual maturities of MBS are affected by the contractual lives of the underlying mortgage collateral, scheduled payments, and unscheduled prepayments of principal, and the payment priority structure of the security; therefore, actual maturities are generally shorter than the securities' stated contractual maturities.

12

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

The following table presents information regarding unrealized gains and losses on investments reported within net income (loss) on the Company’s consolidated statements of comprehensive income (loss) for the periods indicated:

| Three Months Ended | |||||||||||

| March 31, | |||||||||||

($s in thousands) | 2026 | 2025 | |||||||||

| Agency RMBS | $ | ( | $ | ||||||||

| Agency CMBS | ( | ||||||||||

| CMBS IO | ( | ||||||||||

Other investments | ( | ||||||||||

| Unrealized (loss) gain on investments, net | $ | ( | $ | ||||||||

| Three Months Ended | |||||||||||

| March 31, | |||||||||||

($s in thousands) | 2026 | 2025 | |||||||||

Realized gain on sales of MBS - FVO | $ | $ | |||||||||

Realized loss on sale of MBS - FVO | |||||||||||

Total realized gain on sales of investments, net | $ | $ | |||||||||

The following table presents certain information for MBS designated as AFS that were in an unrealized loss position as of the dates indicated:

| March 31, 2026 | December 31, 2025 | |||||||||||||||||||||||||||||||||||||

($s in thousands) | Fair Value | Gross Unrealized Losses | # of Securities | Fair Value | Gross Unrealized Losses | # of Securities | ||||||||||||||||||||||||||||||||

| Continuous unrealized loss position for less than 12 months: | ||||||||||||||||||||||||||||||||||||||

| Agency MBS | $ | $ | ( | $ | $ | ( | ||||||||||||||||||||||||||||||||

| Non-Agency MBS | ( | ( | ||||||||||||||||||||||||||||||||||||

| Continuous unrealized loss position for 12 months or longer: | ||||||||||||||||||||||||||||||||||||||

| Agency MBS | $ | $ | ( | $ | $ | ( | ||||||||||||||||||||||||||||||||

| Non-Agency MBS | ( | ( | ||||||||||||||||||||||||||||||||||||

13

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

NOTE 4 – REPURCHASE AGREEMENTS

The Company’s repurchase agreements outstanding as of March 31, 2026 and December 31, 2025 are summarized in the following tables:

| March 31, 2026 | December 31, 2025 | |||||||||||||||||||||||||||||||||||||

| Collateral Type | Balance | Weighted Average Rate | Fair Value of Collateral Pledged (1) | Balance | Weighted Average Rate | Fair Value of Collateral Pledged (1) | ||||||||||||||||||||||||||||||||

($s in thousands) | ||||||||||||||||||||||||||||||||||||||

| Agency RMBS | $ | % | $ | $ | % | $ | ||||||||||||||||||||||||||||||||

| Agency CMBS | % | % | ||||||||||||||||||||||||||||||||||||

| Agency CMBS IO | % | % | ||||||||||||||||||||||||||||||||||||

| Non-Agency CMBS IO | % | % | ||||||||||||||||||||||||||||||||||||

Total | $ | % | $ | $ | % | $ | ||||||||||||||||||||||||||||||||

(1) Amounts disclosed for fair value of collateral pledged include amounts pledged to cover margin calls, which may differ in collateral type from the initial collateral type pledged.

The Company’s equity at risk did not exceed 10% with any single counterparty as of March 31, 2026.

The following table provides information on the remaining term to maturity and original term to maturity for the Company’s repurchase agreements as of the dates indicated:

| March 31, 2026 | December 31, 2025 | |||||||||||||||||||||||||||||||||||||

| Remaining Term to Maturity | Balance | Weighted Average Rate | WAVG Original Term to Maturity | Balance | Weighted Average Rate | WAVG Original Term to Maturity | ||||||||||||||||||||||||||||||||

($s in thousands) | ||||||||||||||||||||||||||||||||||||||

| Less than 30 days | $ | % | $ | % | ||||||||||||||||||||||||||||||||||

| 30 to 90 days | % | % | ||||||||||||||||||||||||||||||||||||

| 91 to 180 days | % | % | ||||||||||||||||||||||||||||||||||||

| Total | $ | % | $ | % | ||||||||||||||||||||||||||||||||||

The Company’s accrued interest payable related to its repurchase agreement borrowings increased to $131 million as of March 31, 2026 from $95 million as of December 31, 2025.

The Company’s counterparties, as set forth in the master repurchase agreement with each counterparty, require the Company to comply with various customary operating and financial covenants, including, but not limited to, minimum net worth, maximum declines in net worth in a given period, and maximum leverage requirements as well as maintaining the Company’s REIT status. In addition, some of the agreements contain cross default features, whereby default under an agreement with one lender simultaneously causes default under agreements with other lenders. To the extent that the Company fails to comply with the covenants contained in these financing agreements or is otherwise found to be in default under the terms of such agreements, the counterparty has the right to accelerate amounts due under the master repurchase agreement. The Company believes it was in full compliance with all covenants in master repurchase agreements under which there were amounts outstanding as of March 31, 2026.

The Company's repurchase agreements are subject to underlying agreements with master netting or similar arrangements, which provide for the right of set off in the event of default or in the event of bankruptcy of either party to the transactions. The Company reports its repurchase agreements to these arrangements on a gross basis. The following table presents information regarding the Company's repurchase agreements as if the Company had

14

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

presented them on a net basis as of March 31, 2026 and December 31, 2025:

($s in thousands) | Gross Amount of Recognized Liabilities | Gross Amount Offset in the Balance Sheet | Net Amount of Liabilities Presented in the Balance Sheet | Gross Amount Not Offset in the Balance Sheet (1) | Net Amount | ||||||||||||||||||||||||||||||

| Financial Instruments Posted as Collateral | Cash Posted as Collateral | ||||||||||||||||||||||||||||||||||

| March 31, 2026: | |||||||||||||||||||||||||||||||||||

| Repurchase agreements | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

| December 31, 2025: | |||||||||||||||||||||||||||||||||||

| Repurchase agreements | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

(1) Amounts disclosed for collateral received by or posted to the same counterparty include cash and the fair value of MBS up to and not exceeding the net amount of the repurchase agreement liability presented in the balance sheet. The fair value of the total collateral received by or posted to the same counterparty may exceed the amounts presented. Please refer to the consolidated balance sheets for the total fair value of financial instruments pledged as collateral for derivatives and repurchase agreements, which is shown parenthetically, and the total cash pledged or received as collateral, which is disclosed as “cash collateral posted to/by counterparties.”

NOTE 5 – DERIVATIVES

Types and Uses of Derivatives Instruments

Interest Rate Derivatives. The Company frequently changes the type of derivative instruments it uses to mitigate the impact of changing interest rates on its repurchase agreement financing costs and the fair value of its investments. Please refer to Note 1 for descriptions of these instruments and how the Company accounts for them.

TBA Transactions. The Company purchases TBA securities as a means of investing in non-specified fixed-rate Agency RMBS and may also periodically sell TBA securities as a means of economically hedging its exposure to Agency RMBS. Please refer to Note 1 for more information about these securities.

The table below provides detail of the Company’s gain and losses by type of derivative instrument for the periods indicated:

| Three Months Ended | ||||||||||||||

| March 31, | ||||||||||||||

| Type of Derivative Instrument | 2026 | 2025 | ||||||||||||

($s in thousands) | ||||||||||||||

| U.S. Treasury futures | $ | $ | ( | |||||||||||

Interest rate swaps | ( | |||||||||||||

Interest rate swaptions | ( | |||||||||||||

Options on U.S. Treasury futures | ( | |||||||||||||

TBA securities | ( | |||||||||||||

| Gain (loss) on derivative instruments, net | $ | $ | ( | |||||||||||

The table below provides the carrying amount by type of derivative instrument comprising the Company’s derivative assets and liabilities on its consolidated balance sheets as of the dates indicated:

15

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

| Type of Derivative Instrument | Balance Sheet Location | Purpose | March 31, 2026 | December 31, 2025 | ||||||||||||||||||||||

($s in thousands) | ||||||||||||||||||||||||||

Options on U.S. Treasury futures | Derivative assets | Economic hedging | $ | $ | ||||||||||||||||||||||

| TBA securities | Derivative assets | Investing | ||||||||||||||||||||||||

| Total derivatives assets | $ | $ | ||||||||||||||||||||||||

Interest rate swaptions | Derivative liabilities | Economic hedging | $ | $ | ||||||||||||||||||||||

| TBA securities | Derivative liabilities | Investing | ||||||||||||||||||||||||

| Total derivatives liabilities | $ | $ | ||||||||||||||||||||||||

The table below presents information regarding the long positions in SOFR-based interest rate swaptions and options on U.S. Treasury futures held by the Company as of the dates indicated:

Option | Underlying Financial Instrument | ||||||||||||||||||||||||||||||||||

($s in thousands) | Cost (1) | Fair Value | Carrying Value (1) | Notional Amount | Average Fixed Receive Rate | Type of Instrument | |||||||||||||||||||||||||||||

As of March 31, 2026: | |||||||||||||||||||||||||||||||||||

1-2 year interest rate swaptions | $ | $ | $ | ( | $ | 5 year SOFR-based swap | |||||||||||||||||||||||||||||

3-month options on U.S. Treasury futures | n/a | 10-year U.S. Treasury future | |||||||||||||||||||||||||||||||||

| As of December 31, 2025: | |||||||||||||||||||||||||||||||||||

1-2 year interest rate swaptions | $ | $ | $ | ( | $ | 5 year SOFR-based swap | |||||||||||||||||||||||||||||

3-month options on U.S. Treasury futures | n/a | 10-year U.S. Treasury future | |||||||||||||||||||||||||||||||||

(1)The Company pays the premium for its interest rate swaptions at the end of the option period, so the carrying value on the Company's consolidated balance sheets is fair value, net of the payable for the unpaid premium as of the periods indicated. The Company pays the premium for its options on U.S. Treasury futures at inception, so the carrying value is equal to the fair value as of the periods indicated.

Because the daily margin exchanged for the Company’s U.S. Treasury futures and interest rate swaps are considered legal settlement of the derivative as opposed to a pledge of collateral, these instruments have a carrying value of $0 58 million as of March 31, 2026 and a net asset position of $22 million as of December 31, 2025, and its interest rate swaps were in a net asset position of $39 million as of March 31, 2026 and net liability position of $(46 ) million as of December 31, 2025. The amount of cash posted by the Company to cover required initial margin for its U.S. Treasury futures and its interest rate swaps was $486 million as of March 31, 2026 and $392 million as of December 31, 2025, which was recorded within “cash collateral posted to counterparties.” The Company had a margin payable of $26 million as of March 31, 2026 recorded within “due to counterparties” and $17 million as of December 31, 2025 recorded within “due from counterparties.”

The table below presents information regarding the pay fixed/receive variable SOFR-based interest rate swaps the Company held as of the dates indicated:

16

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

| March 31, 2026 | December 31, 2025 | |||||||||||||||||||||||||

Pay Fixed Interest Rate Swaps - Years to Maturity | Notional Amount | Weighted Average Pay Fixed Rate | Notional Amount | Weighted Average Pay Fixed Rate | ||||||||||||||||||||||

($s in thousands) | ||||||||||||||||||||||||||

3-5 years | $ | % | $ | % | ||||||||||||||||||||||

5-7 years | % | % | ||||||||||||||||||||||||

7-10 years | % | % | ||||||||||||||||||||||||

10-15 years | % | % | ||||||||||||||||||||||||

| $ | % | $ | % | |||||||||||||||||||||||

The table below presents information regarding the notional amounts of the short positions in U.S. Treasury futures held by the Company as of the dates indicated:

U.S. Treasury Futures | March 31, 2026 | December 31, 2025 | ||||||||||||

($s in thousands) | ||||||||||||||

| 5-year U.S. Treasury futures | $ | $ | ( | |||||||||||

10-year U.S. Treasury futures | ( | ( | ||||||||||||

30-year U.S. Treasury futures | ( | ( | ||||||||||||

| $ | ( | $ | ( | |||||||||||

The following table summarizes information about the notional amounts of the Company's long positions in TBA securities as of the dates indicated:

| TBA securities | March 31, 2026 | December 31, 2025 | ||||||||||||

| ($s in thousands) | ||||||||||||||

Implied market value (1) | $ | $ | ||||||||||||

Implied cost basis (2) | ||||||||||||||

Net carrying value (3) | $ | ( | $ | |||||||||||

(1) Implied market value represents the estimated fair value of the underlying Agency MBS as of the dates indicated .

(2) Implied cost basis represents the forward price to be paid for the underlying Agency MBS as of the dates indicated.

(3) Net carrying value represents the difference between the implied market value and the implied cost basis of the Company’s TBA securities as of the dates indicated. The total shown is the net amount included on the consolidated balance sheets as derivative assets of $695 and derivative liabilities of $9,741 as of March 31, 2026 and $7,841 and $785 , respectively, as of December 31, 2025.

Volume of Activity

The table below summarizes changes in the Company’s derivative instruments for the three months ended March 31, 2026:

| Type of Derivative Instrument | Beginning Notional Amount-Long (Short) | Additions | Settlements, Terminations, or Pair-Offs | Ending Notional Amount-Long (Short) | ||||||||||||||||||||||

($s in thousands) | ||||||||||||||||||||||||||

| U.S. Treasury futures | $ | ( | $ | ( | $ | $ | ( | |||||||||||||||||||

Interest rate swaps | ( | |||||||||||||||||||||||||

Interest rate swaptions | — | |||||||||||||||||||||||||

Options on U.S. Treasury futures | ( | |||||||||||||||||||||||||

| TBA securities | ( | |||||||||||||||||||||||||

17

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Offsetting

The Company's derivatives are subject to underlying agreements with master netting or similar arrangements, which provide for the right of set off in the event of default or in the event of bankruptcy of either party to the transactions. The Company reports its derivative assets and liabilities subject to these arrangements on a gross basis. Please see Note 4 for information related to the Company’s repurchase agreements, which are also subject to underlying agreements with master netting or similar arrangements. The following tables present information regarding those derivative assets and liabilities subject to such arrangements as if the Company had presented them on a net basis as of March 31, 2026 and December 31, 2025:

| Offsetting of Assets | |||||||||||||||||||||||||||||||||||

($s in thousands) | Gross Amount of Recognized Assets | Gross Amount Offset in the Balance Sheet | Net Amount of Assets Presented in the Balance Sheet | Gross Amount Not Offset in the Balance Sheet (1) | Net Amount | ||||||||||||||||||||||||||||||

| Financial Instruments Received as Collateral | Cash Received as Collateral | ||||||||||||||||||||||||||||||||||

| March 31, 2026 | |||||||||||||||||||||||||||||||||||

| TBA securities | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||||

| Derivative assets | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

| December 31, 2025 | |||||||||||||||||||||||||||||||||||

Options on U.S. Treasury futures | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| TBA securities | ( | ( | |||||||||||||||||||||||||||||||||

| Derivative assets | $ | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||

| Offsetting of Liabilities | |||||||||||||||||||||||||||||||||||

($s in thousands) | Gross Amount of Recognized Liabilities | Gross Amount Offset in the Balance Sheet | Net Amount of Liabilities Presented in the Balance Sheet | Gross Amount Not Offset in the Balance Sheet (1) | Net Amount | ||||||||||||||||||||||||||||||

| Financial Instruments Posted as Collateral | Cash Posted as Collateral | ||||||||||||||||||||||||||||||||||

| March 31, 2026 | |||||||||||||||||||||||||||||||||||

Interest rate swaptions | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| TBA securities | ( | ( | |||||||||||||||||||||||||||||||||

| Derivative liabilities | $ | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||

| December 31, 2025 | |||||||||||||||||||||||||||||||||||

Interest rate swaptions | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| TBA securities | ( | ( | |||||||||||||||||||||||||||||||||

| Derivative liabilities | $ | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||

(1)Amounts disclosed for collateral received by or posted to the same counterparty include cash and the fair value of MBS up to and not exceeding the net amount of the derivative asset or liability presented in the balance sheet. The fair value of the total collateral received by or posted to the same counterparty may exceed the amounts presented. Please refer to the consolidated balance sheets for the total fair value of financial instruments pledged as collateral for derivatives and repurchase agreements, which is shown parenthetically, and the total cash pledged or received as collateral which is disclosed as “cash collateral posted to/by counterparties.”

18

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

NOTE 6 – FAIR VALUE OF FINANCIAL INSTRUMENTS

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Fair value is based on the assumptions market participants would use when pricing an asset or liability and also considers all aspects of nonperformance risk, including the entity’s own credit standing, when measuring fair value of a liability. ASC Topic 820 established a valuation hierarchy of three levels as follows:

•Level 1 – Inputs are unadjusted, quoted prices in active markets for identical assets or liabilities as of the measurement date.

•Level 2 – Inputs include quoted prices in active markets for similar assets or liabilities; quoted prices in inactive markets for identical or similar assets or liabilities; or inputs either directly observable or indirectly observable through correlation with market data at the measurement date and for the duration of the instrument’s anticipated life.

•Level 3 – Unobservable inputs are supported by little or no market activity. The unobservable inputs represent management’s best estimate of how market participants would price the asset or liability at the measurement date. Consideration is given to the risk inherent in the valuation technique and the risk inherent in the inputs to the model.

The following table presents the Company’s financial instruments that are measured at fair value on the Company’s consolidated balance sheet by their valuation hierarchy levels as of the dates indicated:

($s in thousands) | March 31, 2026 | December 31, 2025 | |||||||||||||||||||||||||||||||||||||||||||||

Total | Level 1 | Level 2 | Level 3 | Total | Level 1 | Level 2 | Level 3 | ||||||||||||||||||||||||||||||||||||||||

Assets: | |||||||||||||||||||||||||||||||||||||||||||||||

| MBS | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

TBA securities (1) | |||||||||||||||||||||||||||||||||||||||||||||||

Option on U.S. Treasury futures | |||||||||||||||||||||||||||||||||||||||||||||||

Mortgage loans (2) | |||||||||||||||||||||||||||||||||||||||||||||||

Total | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

Liabilities: | |||||||||||||||||||||||||||||||||||||||||||||||

TBA securities (1) | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

Interest rate swaptions (3) | |||||||||||||||||||||||||||||||||||||||||||||||

Total | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

(1)TBA securities are reflected on the consolidated balance sheet as derivative assets or liabilities at their implied fair value, net of implied cost basis. Please refer to Note 5 for additional information .

(2)Mortgage loans are included on the consolidated balance sheets as a component of other assets.

The fair value measurements for the Company’s TBA securities and its MBS are considered Level 2 because there are substantially similar securities actively trading or for which there has been recent trading activity in their respective markets. Fair value for Agency MBS and TBA securities is based on prices received from an independent third-party pricing service. In valuing a security, the pricing service primarily uses a market approach, which uses observable prices and other relevant information that is generated by market transactions of identical or

19

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

similar securities, but may use an income approach, which uses valuation techniques such as discounted cash flow modeling. Examples of the observable inputs and assumptions used in the valuation techniques include market interest rates, credit spreads, and projected prepayment speeds, among other things. The Company reviews the prices it receives from the pricing service for reasonableness using other third-party pricing services. If the fair value of a security is not available from a third-party pricing service, the Company may estimate the fair value of the security through a variety of methods using observable market data.

The Company's mortgage loans held for investment are single-family mortgage loans, which were originated or purchased by the Company prior to 2000, and for which the Company has elected the fair value option. The fair value measurements for these mortgage loans are considered Level 3 because there has been no recent trading activity of similar instruments upon which their fair value can be measured. The fair value for these Level 3 assets is measured by discounting the estimated future cash flows derived from cash flow models using certain inputs such as the security’s credit rating, coupon rate, estimated prepayment speeds, expected weighted average life, collateral composition, and expected credit losses as well as certain other relevant information. The Company used a constant prepayment rate assumption of 10 2 20 10

The Company’s short positions in U.S. Treasury futures contracts are valued based on exchange pricing and are classified accordingly as Level 1 measurements. Interest rate swaps are valued using the daily settlement price, or fair value, determined by the clearing exchange based on a pricing model that references observable market inputs, including current benchmark rates and the forward yield curve, and thus their fair values are considered Level 2 measurements. The carrying value of the U.S. Treasury futures contracts and interest rate swaps on the Company’s consolidated balance sheets is $0

The fair value measurement of interest rate swaptions is considered Level 2 because it is based on the fair value of the underlying interest rate swap and time remaining until its expiration and is carried on the balance sheet net of any deferred premium to be paid upon exercise or expiration. The fair value measurement of options on U.S. Treasury futures is considered Level 1 because they are valued based on closing exchange prices on these contracts. Options on U.S. Treasury futures are initially recorded on the balance sheet at the contract price paid and subsequently adjusted for changes in fair value until exercise or expiration.

NOTE 7 – SHAREHOLDERS’ EQUITY AND SHARE-BASED COMPENSATION

Preferred Stock. The Company’s Board of Directors has designated 6,600,000 shares of the Company’s preferred stock for issuance as Series C Preferred Stock, of which the Company has 4,460,000 of such shares outstanding as of March 31, 2026. The Series C Preferred Stock has no stated maturity, is not subject to any sinking fund or mandatory redemption, and will remain outstanding indefinitely unless redeemed, repurchased, or converted into common stock pursuant to the terms of the Series C Preferred Stock. As of April 15, 2025, the Series C Preferred Stock may be redeemed at any time and from time to time at the Company's option at a cash redemption price of $25.00 per share plus any accumulated and unpaid dividends. In addition, the Series C Preferred Stock will now pay a quarterly cumulative cash dividend at a percentage of its $25.00 liquidation value per share equal to 3-month term SOFR plus the statutorily prescribed tenor spread adjustment of 0.26161 % in addition to the spread pursuant to the terms of the Series C Preferred Stock of 5.461 % for a total spread of 5.723 %. The Company paid a quarterly dividend of $0.58711 per share of Series C Preferred Stock on April 15, 2026 to shareholders of record as

20

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

of April 1, 2026.

Common Stock. During the three months ended March 31, 2026, the Company issued 32,101,365 shares of its common stock through its at-the-market (“ATM”) program at an aggregate value of $442 million, net of broker commissions and fees. The Company declared monthly dividends on its common stock totaling $0.51 for the three months ended March 31, 2026. The Company’s timing, frequency, and amount of dividends declared on its common stock are determined by its Board of Directors. When declaring dividends, the Board of Directors considers the Company’s taxable income, management’s view on long-term returns, the REIT distribution requirements of the Tax Code, and maintaining compliance with dividend requirements of the Series C Preferred Stock, along with other factors that the Board of Directors may deem relevant from time to time.

Share-Based Compensation. The following table presents a rollforward of share-based awards for the periods indicated:

| Three Months Ended | ||||||||||||||||||||||||||

| March 31, | ||||||||||||||||||||||||||

| 2026 | 2025 | |||||||||||||||||||||||||

| Type of Award | Shares | Weighted Average Grant Date Fair Value Per Share | Shares | Weighted Average Grant Date Fair Value Per Share | ||||||||||||||||||||||

| Restricted stock: | ||||||||||||||||||||||||||

| Awards outstanding, beginning of period | $ | $ | ||||||||||||||||||||||||

| Granted | ||||||||||||||||||||||||||

| Vested | ( | ( | ||||||||||||||||||||||||

| Awards outstanding, end of period | $ | $ | ||||||||||||||||||||||||

Target RSUs: (1) | ||||||||||||||||||||||||||

| Awards outstanding, beginning of period | $ | $ | ||||||||||||||||||||||||

| Granted | ||||||||||||||||||||||||||

| Vested | ( | ( | ||||||||||||||||||||||||

| Awards outstanding, end of period | $ | $ | ||||||||||||||||||||||||

Target PSUs: (2) | ||||||||||||||||||||||||||

| Awards outstanding, beginning of period | $ | $ | ||||||||||||||||||||||||

| Granted | ||||||||||||||||||||||||||

| Vested | ||||||||||||||||||||||||||

| Awards outstanding, end of period | $ | $ | ||||||||||||||||||||||||

(1)The number of RSUs shown represent the target number of awards. Actual number of shares that will potentially settle may range from 0 % if the recipient’s service-based vesting condition is not met to 100 % if the service-based vesting condition is met.

(2)The number of PSUs shown represent the target number of awards. Actual number of shares that will potentially settle may range from 0 % to 200 % based on the achievement of the performance goals defined in each grant award.

Restricted stock granted to employees generally vests in equal installments over a period of 3 years. RSUs generally vest in equal installments over a period of 3 years if granted to employees and one year if granted to a non-employee director. PSUs cliff vest based on performance results measured over a period of 3 years. The Company expects 130 % of the remaining target PSUs outstanding as of March 31, 2026 will be settled on their vesting dates.

21

DYNEX CAPITAL, INC.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

The following table discloses the dividends payable to the Company’s shareholders for common and preferred stock as well as to its employees and directors for DERs related to its outstanding RSUs and PSUs as of the dates indicated:

Dividends Payable | March 31, 2026 | December 31, 2025 | ||||||||||||

| ($s in thousands) | ||||||||||||||

| RSU DERs | $ | $ | ||||||||||||

| PSU DERs | ||||||||||||||

Accrued DERs | ||||||||||||||

Common stock dividends | $ | $ | ||||||||||||

Preferred stock dividends | ||||||||||||||

Accrued dividends | ||||||||||||||

| Total dividends payable | $ | $ | ||||||||||||

Total share-based compensation expense recognized by the Company for the three months ended March 31, 2026 was $8 million compared to $2 million for the three months ended March 31, 2025. The following table discloses the Company’s remaining compensation expense related to stock awards it has granted as of March 31, 2026, which will be amortized over the period disclosed:

| March 31, 2026 | |||||||||||

($s in thousands) | Remaining Compensation Cost | WAVG Period of Recognition | |||||||||

| Restricted stock | $ | ||||||||||

| RSUs | |||||||||||

| PSUs | |||||||||||

| Total | $ | ||||||||||

NOTE 8 - SEGMENT REPORTING

The Company’s operations consist of one reportable segment which involves investing in MBS and funding these investments with repurchase agreements and equity. Because the Company’s investment portfolio and financings are subject to market risks, primarily interest rate risk, management seeks to offset a portion of its market value exposure and financing costs through its interest rate derivative instruments (“hedging portfolio”). The Company’s investment and hedging portfolios are managed together.

NOTE 9 - SUBSEQUENT EVENTS

22

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

EXECUTIVE OVERVIEW

During the first quarter of 2026, financial markets experienced increased volatility as investors reassessed the outlook for inflation, monetary policy, and global growth amid heightened geopolitical uncertainty. While the U.S. economy continued to expand at a moderate pace, uncertainty around the inflation trajectory led market participants to reduce expectations for near‑term Federal Reserve policy easing. Funding markets remained orderly, and liquidity across the mortgage and repo markets continued to function effectively. Spreads across Agency MBS widened meaningfully, particularly late in the quarter, as periodic correlation with risky assets increased amid macroeconomic and geopolitical developments.

Against this backdrop, Agency MBS continues to offer attractive long‑term return potential relative to other high‑quality fixed‑income assets, particularly given muted new mortgage origination supply and the sector’s strong liquidity profile. We continue to monitor monetary policy, inflation trends, housing market activity, supply‑and‑demand dynamics, and geopolitical developments, as we assess their potential impact on interest rates, spreads, prepayment behavior, and financing conditions. We remain focused on disciplined portfolio construction, liquidity management, and risk positioning as market conditions continue to evolve.

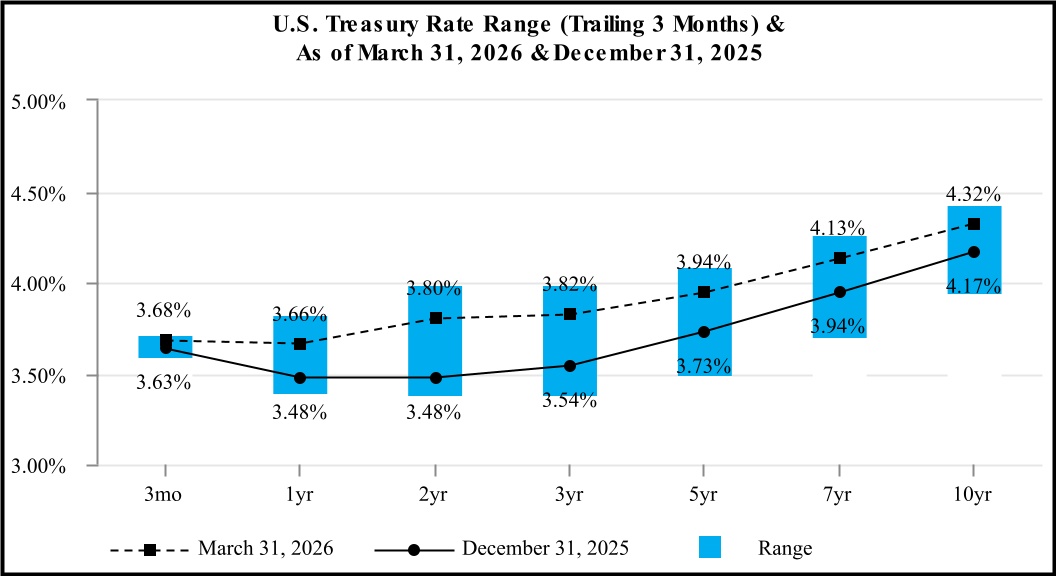

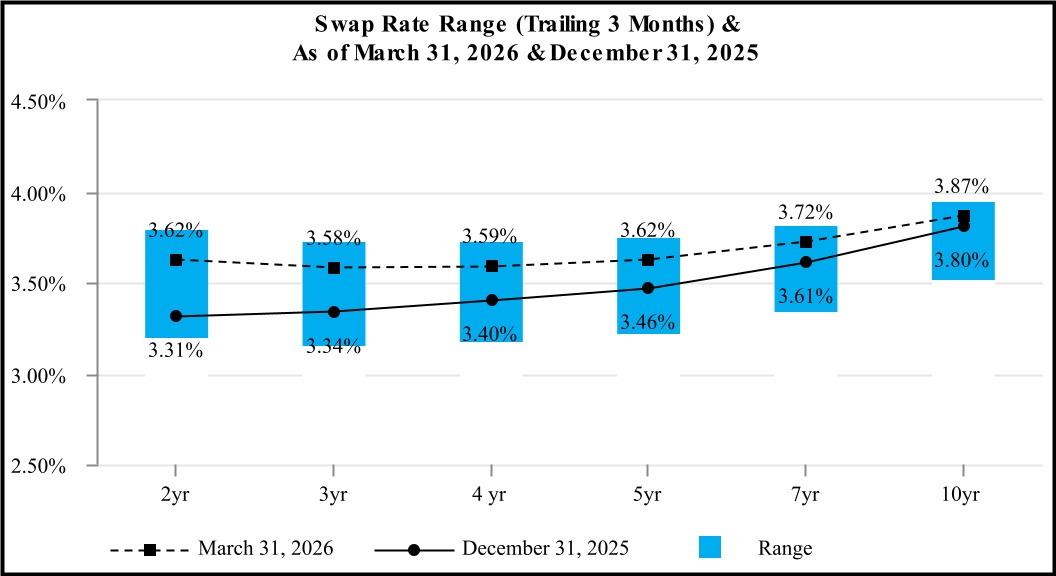

The charts below show the range of U.S. Treasury and Secured Overnight Funding Rate (“SOFR”)-based swap rates for the three months ended March 31, 2026 and information regarding market spreads as of and for the periods indicated:

23

Market Spreads as of: | Change in Spreads YTD | |||||||||||||||||||

Investment Type: (1) | March 31, 2026 | December 31, 2025 | ||||||||||||||||||

Agency RMBS: | ||||||||||||||||||||

| 2.0% coupon | 73 | 70 | 3 | |||||||||||||||||

| 2.5% coupon | 76 | 73 | 3 | |||||||||||||||||

| 4.0% coupon | 52 | 50 | 2 | |||||||||||||||||

| 4.5% coupon | 53 | 45 | 8 | |||||||||||||||||

| 5.0% coupon | 56 | 46 | 10 | |||||||||||||||||

| 5.5% coupon | 63 | 51 | 12 | |||||||||||||||||

| 6.0% coupon | 64 | 54 | 10 | |||||||||||||||||

Agency CMBS(2) | 84 | 82 | 2 | |||||||||||||||||

(1)Option adjusted spreads (“OAS”) are based on Company estimates using third-party models and market data. OAS shown for prior periods may differ from previous disclosures because the Company regularly updates the third-party model used.

(2)Data is sourced from J.P. Morgan and represents the spread to swap rate on newly issued Agency securities collateralized by multifamily properties.

Summary of First Quarter 2026 Financial Performance

For the first quarter of 2026, our total economic return of $(0.34) per common share was comprised of a decrease in book value of $(0.85) per common share offset by dividends declared of $0.51 per common share. The decrease in book value per common share was driven by a net loss of $(140) million on our investment portfolio, net of hedges, which resulted primarily from widening mortgage spreads late in the quarter. We grew our capital base by $442 million, using the proceeds to opportunistically add investments of $6 billion, net of sales. Our adjusted leverage increased to 8.6 times equity primarily due to our use of repurchase agreement borrowings to partially finance these purchases.

Our interest income continued to increase as a result of our deployment of capital into Agency MBS purchases over recent quarters. In addition, the Federal Reserve's rate cuts in 2025 continued to benefit our repurchase agreement financing costs, which declined 33 basis points for the first quarter of 2026 compared to the prior quarter. Operating expenses for the first quarter of 2026 included an increase of $3.4 million in share-based compensation expense, largely due to accelerated vesting conditions for equity grants associated with the departure of the Company's former chief financial officer.

24

The following table summarizes the changes in the Company's financial position during the three months ended March 31, 2026:

($s in thousands except per share data) | Net Change in Fair Value | Components of Comprehensive Income | Common Book Value Rollforward | Per Common Share | |||||||||||||||||||

Balance as of December 31, 2025 (1) | $ | 2,350,644 | $ | 13.45 | |||||||||||||||||||

Net interest income | $ | 79,254 | |||||||||||||||||||||

Periodic interest from interest rate swaps | 1,698 | ||||||||||||||||||||||

| G & A and other operating expenses | (21,253) | ||||||||||||||||||||||

| Preferred stock dividends | (2,658) | ||||||||||||||||||||||

| Changes in fair value: | |||||||||||||||||||||||

MBS and other | $ | (243,238) | |||||||||||||||||||||

| TBAs | (13,879) | ||||||||||||||||||||||

| U.S. Treasury futures | 35,308 | ||||||||||||||||||||||

Options on U.S. Treasury futures | (2,656) | ||||||||||||||||||||||

Interest rate swaps | 84,591 | ||||||||||||||||||||||

Interest rate swaptions | (335) | ||||||||||||||||||||||

| Total net change in fair value | (140,209) | ||||||||||||||||||||||

Comprehensive loss to common shareholders | (83,168) | ||||||||||||||||||||||

| Capital transactions: | |||||||||||||||||||||||

Net proceeds from stock issuance (2) | 446,903 | ||||||||||||||||||||||

| Common dividends declared | (104,609) | ||||||||||||||||||||||

Balance as of March 31, 2026 (1) | $ | 2,609,770 | $ | 12.60 | |||||||||||||||||||

(1)Amounts represent total shareholders' equity less the aggregate liquidation preference of the Company's preferred stock of $111.5 million, in thousands and on a per common share basis.

(2)Net proceeds from common stock issuance include approximately $442 million from ATM issuances and approximately $5 million from amortization of share-based compensation, net of grants, during the three months ended March 31, 2026.

25

FINANCIAL CONDITION

Investment Portfolio

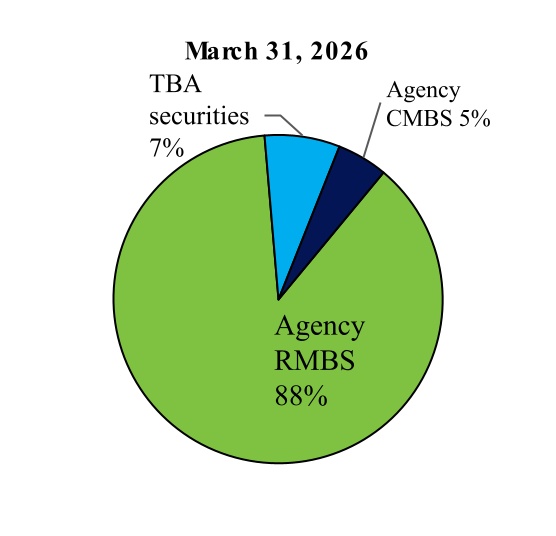

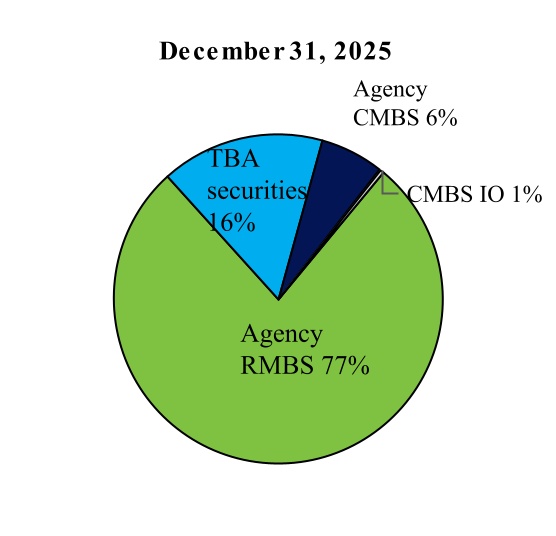

Our investment portfolio, including TBAs, as of March 31, 2026, has increased $6 billion, or 27%, since December 31, 2025, net of sales. We added over $7 billion of Agency RMBS, net of sales of $608 million, during the three months ended March 31, 2026. We reduced our TBA securities by a net notional of $1.3 billion. The following charts compare the composition of our investment portfolio as of the dates indicated:

The following tables compare our 30-year fixed-rate Agency RMBS investments, including TBA dollar roll positions, as of the dates indicated:

| March 31, 2026 | ||||||||||||||||||||||||||||||||||||||||||||

Agency RMBS by Coupon | Par/Notional | Amortized Cost/ Implied Cost Basis (3)(5) | Fair Value (4)(5) | Weighted Average | ||||||||||||||||||||||||||||||||||||||||

Loan Age (in months)(6) | 3 Month CPR (6)(7) | Estimated Duration (8) | Market Yield (9) | |||||||||||||||||||||||||||||||||||||||||

| ($s in thousands) | ||||||||||||||||||||||||||||||||||||||||||||

| 2.0% | $ | 1,275,957 | $ | 1,164,966 | $ | 1,041,759 | 68 | 2.2 | % | 7.43 | 4.75 | % | ||||||||||||||||||||||||||||||||

| 2.5% | 648,281 | 646,466 | 554,603 | 65 | 4.6 | % | 6.97 | 4.76 | % | |||||||||||||||||||||||||||||||||||

| 4.0% | 286,550 | 286,876 | 272,829 | 60 | 6.4 | % | 5.86 | 4.81 | % | |||||||||||||||||||||||||||||||||||

4.5% (1) | 1,685,062 | 1,636,907 | 1,636,567 | 36 | 6.7 | % | 5.51 | 4.96 | % | |||||||||||||||||||||||||||||||||||

| 5.0% | 7,479,116 | 7,434,011 | 7,420,134 | 13 | 3.9 | % | 5.01 | 5.11 | % | |||||||||||||||||||||||||||||||||||

| 5.5% | 9,038,565 | 9,145,191 | 9,152,542 | 12 | 8.4 | % | 3.83 | 5.28 | % | |||||||||||||||||||||||||||||||||||

| 6.0% | 1,494,282 | 1,537,251 | 1,538,780 | 11 | 14.8 | % | 2.72 | 5.40 | % | |||||||||||||||||||||||||||||||||||

TBA 4.5%(2) | 1,257,000 | 1,230,544 | 1,227,574 | n/a | n/a | 4.63 | 4.90 | % | ||||||||||||||||||||||||||||||||||||

| TBA 5.0% | 603,000 | 600,548 | 594,473 | n/a | n/a | 4.91 | 5.20 | % | ||||||||||||||||||||||||||||||||||||

| Total | $ | 23,767,813 | $ | 23,682,760 | $ | 23,439,261 | 19 | 6.8 | % | 4.59 | 5.15 | % | ||||||||||||||||||||||||||||||||

| December 31, 2025 | ||||||||||||||||||||||||||||||||||||||||||||

Agency RMBS by Coupon | Par/Notional | Amortized Cost/ Implied Cost Basis (3)(5) | Fair Value (4)(5) | Weighted Average | ||||||||||||||||||||||||||||||||||||||||

Loan Age (in months)(6) | 3 Month CPR (6)(7) | Estimated Duration (8) | Market Yield (9) | |||||||||||||||||||||||||||||||||||||||||

| ($s in thousands) | ||||||||||||||||||||||||||||||||||||||||||||

| 2.0% | $ | 603,965 | $ | 613,475 | $ | 497,097 | 63 | 5.2 | % | 7.42 | 4.68 | % | ||||||||||||||||||||||||||||||||

| 2.5% | 516,325 | 535,039 | 444,904 | 64 | 5.1 | % | 7.02 | 4.67 | % | |||||||||||||||||||||||||||||||||||

| 4.0% | 293,073 | 293,432 | 281,889 | 57 | 6.5 | % | 5.89 | 4.63 | % | |||||||||||||||||||||||||||||||||||

4.5% (1) | 1,911,130 | 1,853,757 | 1,881,304 | 33 | 5.8 | % | 5.46 | 4.74 | % | |||||||||||||||||||||||||||||||||||

| 5.0% | 3,974,655 | 3,913,622 | 3,997,537 | 21 | 5.9 | % | 4.62 | 4.91 | % | |||||||||||||||||||||||||||||||||||

| 5.5% | 6,325,638 | 6,361,758 | 6,465,769 | 13 | 8.1 | % | 3.39 | 5.10 | % | |||||||||||||||||||||||||||||||||||

| 6.0% | 1,381,567 | 1,419,727 | 1,432,860 | 9 | 8.2 | % | 2.28 | 5.14 | % | |||||||||||||||||||||||||||||||||||

| TBA 4.0% | 1,162,000 | 1,101,441 | 1,102,764 | n/a | n/a | 6.29 | 4.76 | % | ||||||||||||||||||||||||||||||||||||